What is BAC (Budget at Completion) in Project Management?

Change management in project management is the structured use of tools, processes, and leadership to manage how changes affect projects, teams, and stakeholders. It combines overseeing project work with supporting people through transitions, ensuring changes are understood, accepted, and adopted while minimizing disruption and helping projects achieve their intended goals successfully.

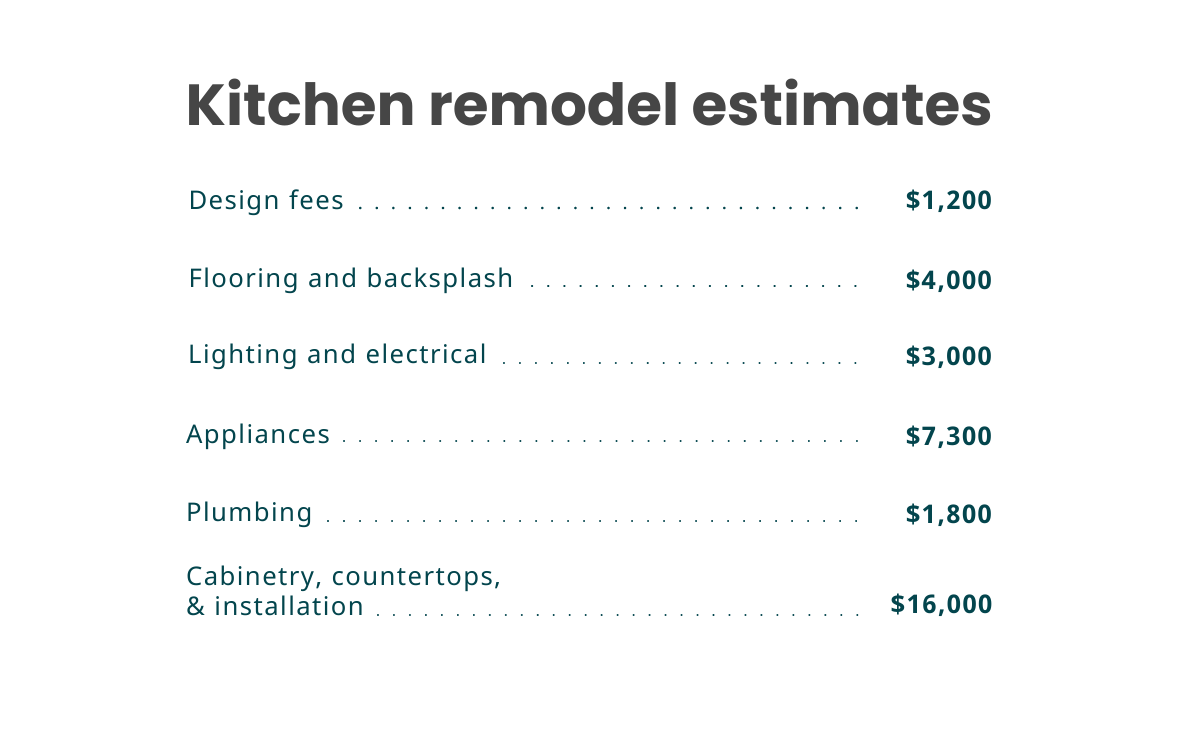

A cost-benefit analysis in project management compares a project’s expected benefits to its total costs to determine whether it’s worth pursuing. It gives teams a clear, data-backed view of a project’s financial viability by quantifying costs, forecasting benefits, and calculating metrics like ROI and NPV. This helps decision makers prioritize initiatives and allocate resources with confidence.

Cost control in project management is the process of monitoring and managing project expenses to make sure the work stays within budget. It includes tracking spending, planning for financial risks, and preparing for potential setbacks that could drive unexpected costs. Effective cost control helps teams avoid overruns, stay on schedule, and use resources more efficiently.

Cost management in project management requires estimating, budgeting, and controlling project expenses so that the work can stay financially on track. Teams can predict future costs, monitor spending throughout the project lifecycle, and compare planned versus actual costs to improve future budgeting. Effective cost management helps prevent overruns, reduce risk, and support better resource planning and long-term profitability.

Cost variance is a measure of a project’s financial performance that compares the budgeted cost of work performed (BCWP) with the actual cost of work performed (ACWP). It shows whether a project is over or under budget, helping teams track spending as the project progresses. A variance close to zero is ideal, though difficult to achieve in practice.